Index Analysis

Our latest Market Snapshot examines emissions trends across the NZ50 index. It shows the real progress that can be made if investment is focused on decarbonisation. However, it also highlights the transition difficulties faced by sectors that do not yet have scalable low carbon technology.

Key Findings:

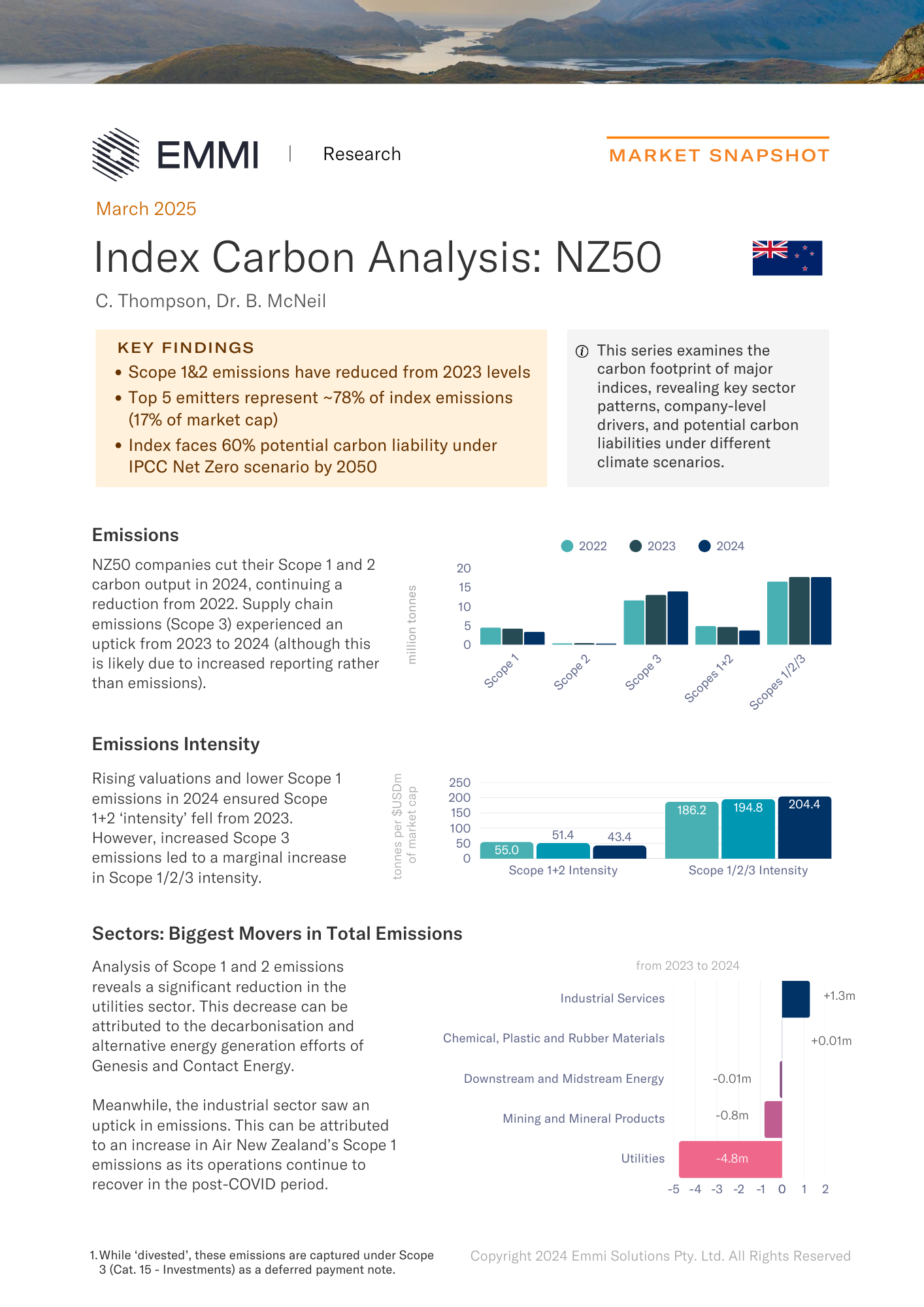

- Scope 1&2 emissions have reduced from 2023 levels

- Top 5 emitters represent ~78% of index emissions (17% of market cap)

- Index faces 60% potential carbon liability under IPCC Net Zero scenario by 2050

NZ50 companies cut their Scope 1 and 2 carbon output in 2024, continuing a reduction from 2022.

This reflects significant decarbonisation efforts and moves into alternative energy generation by Genesis and Contact Energy. This is meaningful for investors seeking to support the transition, but who are in two minds about whether investment in the energy sector is the right thing to do from an ESG or transition risk point of view.

For investors and the economy of New Zealand, the national carrier is important. However, its weight in this relatively small index brings with it difficult choices for markets.

Our analysis also considers the financial and risk implications for these hard-to-abate sectors. Key differences in scenario methodologies being used by markets and in regulatory reporting cause widely divergent transition risk pathways.

Download the full document

Stay in the know. Subscribe to updates

Find out about our latest developments, and get our research reports first.