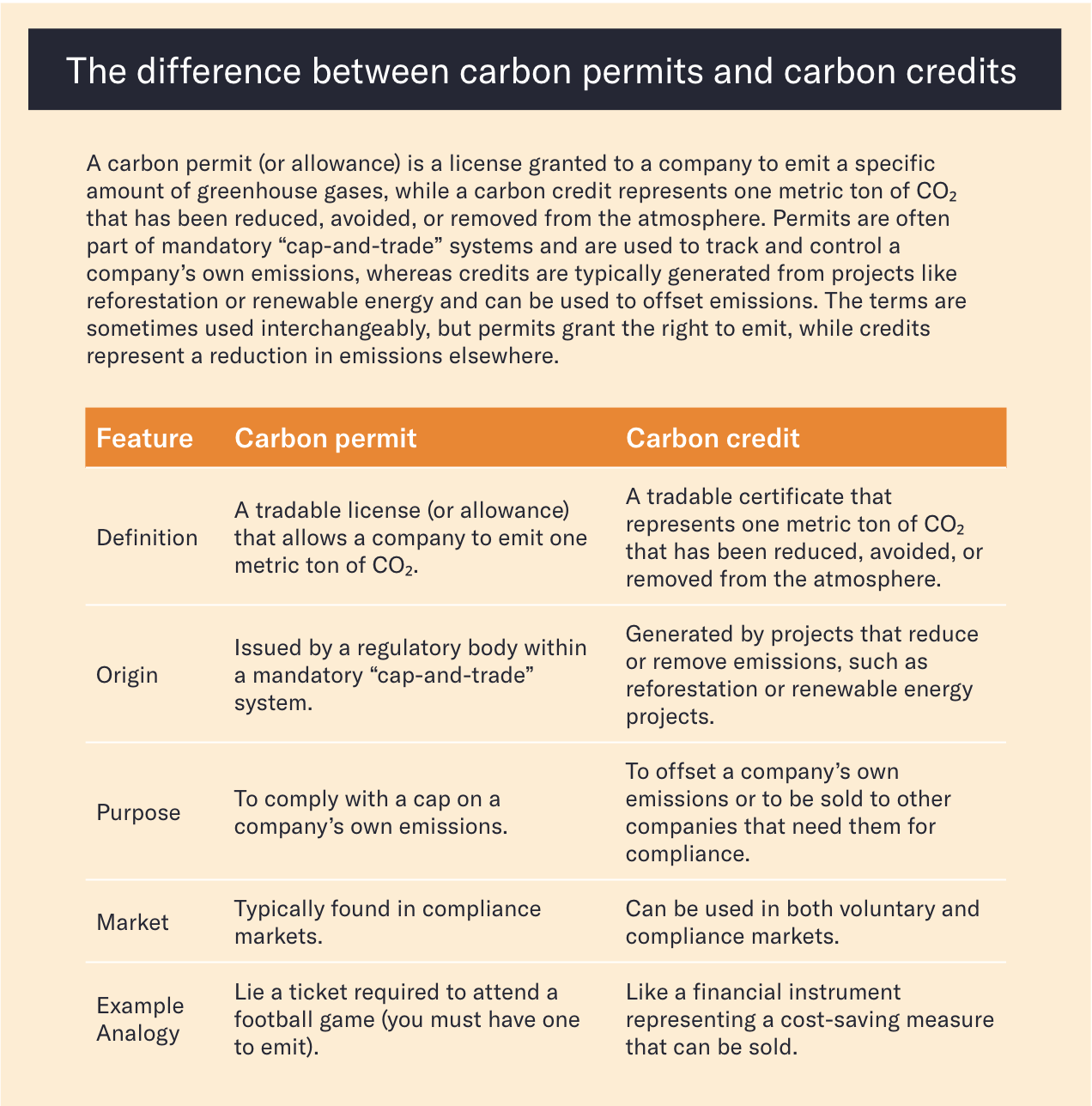

Carbon Instruments

Carbon Credits

Executive Summary

The rapid acceleration of global decarbonisation policies is reshaping investment fundamentals.

For institutional investors, carbon risk, the financial exposure created by rising carbon prices and tightening emissions rules, has become a measurable driver of portfolio value. Governments in Europe, the United Kingdom, Australia and across the world are expanding emissions-trading systems, while new border-adjustment mechanisms and disclosure standards embed carbon costs directly into corporate performance.

In this environment, understanding and managing transition risk is no longer optional. Portfolios with high emissions intensity face structural devaluation as the cost of carbon increases. Yet many investors cannot divest immediately or rely solely on companies’ near-term abatement. This is where carbon credits can play a complementary role, not as a substitute for decarbonisation, but as a strategic instrument for managing exposure, improving temperature alignment, and demonstrating fiduciary diligence.

Drawing on analytics from Carbon Diagnostics and a live case study with Apostle Funds Management, this paper explores how compliance-market carbon credits can hedge portfolio transition risk. It explains the structure of global carbon markets, outlines the distinction between avoidance and removal credits, and demonstrates how investors can integrate credit positions into risk frameworks that align with net-zero commitments.

The message is clear: portfolios prepared for a carbon-constrained world will be more resilient, more compliant, and better positioned to capture the opportunities of the transitioned economy.

1.0 The Rising Importance of Carbon Risk

For over a decade, climate discussions focused primarily on physical risks (storms, droughts, and floods) that directly damage assets and disrupt supply chains. However, as regulation tightens and the understanding of climate-related financial risk matures, transition risk has become a central concern for diversified investors. Transition risk captures the economic costs of adjusting to a low-carbon economy, driven by policy, technology, market, and reputational forces that re-price carbon-intensive assets and reshape portfolio valuations.

Institutional investors are particularly exposed. Across both public and private markets, from listed equities and corporate bonds to private infrastructure and real assets, valuations increasingly reflect assumptions about future carbon prices and regulatory trajectories. As carbon pricing spreads globally, covering nearly 28% of greenhouse-gas emissions and generating over US$100 billion in annual revenues according to the World Bank State and Trends of Carbon Pricing 2025, the implicit cost of carbon within portfolios is becoming explicit.

1.1 Why this matters for investors

Portfolio transition risk can manifest in multiple ways:

- Valuation compression as future carbon liabilities are priced in,

- Earnings risk for companies without credible decarbonisation pathways,

- Cost-of-capital differentials as lenders and insurers price transition exposure, and

- Reputational and legal pressure to demonstrate credible net-zero alignment.

Traditional mitigation strategies, divestment [How to shrink climate risk not returns] or company engagement, remain essential but can be slow, incomplete, or constrained by investment mandates. Many investors face the dilemma of needing to hold carbon-intensive assets while wanting to reduce portfolio exposure. Carbon credits (referring to compliance-market permits or allowances used for hedging, not voluntary offsets), when used prudently, offer a financial instrument to bridge this gap.

Emmi’s work with institutional clients demonstrates that by combining scenario analysis, temperature-alignment metrics, and carbon-price sensitivity, investors can quantify potential value erosion under various scenarios, a concept Emmi terms Potential Carbon Liability (PCL). Once quantified, that liability can be partially offset by exposure to assets whose value rises with carbon prices: regulated carbon credits.

This approach reframes carbon credits from a reputational gesture into a risk-management tool.

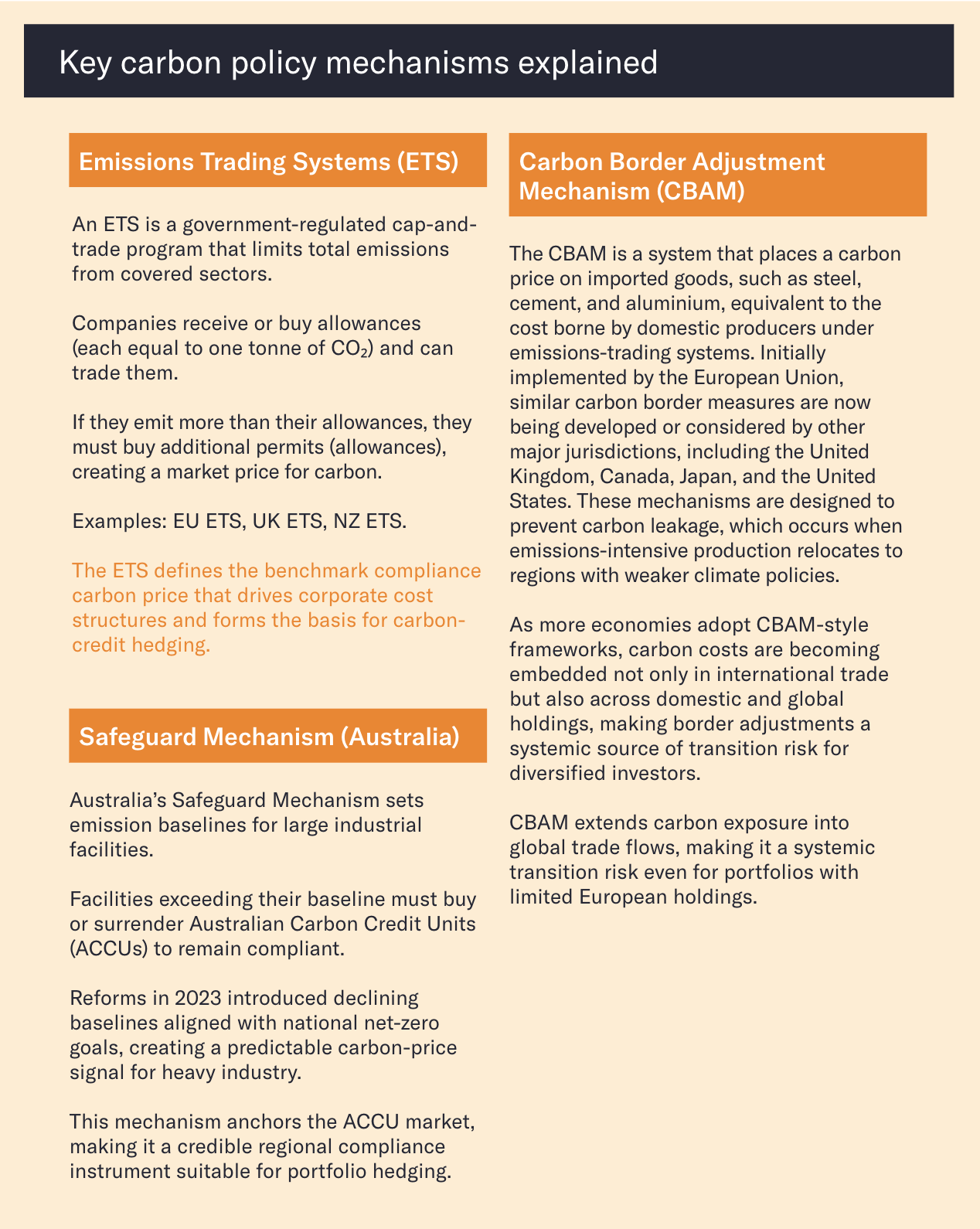

2.0 Carbon Markets and the Price of Transition

Carbon markets are now among the fastest-growing financial ecosystems in the world. In 2024, more than 80 carbon-pricing instruments operated globally, with Europe, the United Kingdom, China, and Australia at the forefront of policy innovation. Prices in the EU Emissions Trading System (EU ETS) have fluctuated between €70–100 per tonne, the UK ETS between £40–70, China’s National ETS around CNY 60–80 (USD 8–11), and Australian Carbon Credit Units (ACCUs) around A$30–40, levels that materially affect company cash flows and investor valuations.

2.1 The policy leaders

- Europe remains a key anchor of global carbon policy. The EU ETS currently covers power, industry, and maritime transport, with ETS 2 set to extend to buildings and road transport by 2027. The Carbon Border Adjustment Mechanism (CBAM) will further embed carbon pricing into trade flows.

- United Kingdom reforms its ETS to tighten the cap by 30% by 2030 and plans a domestic CBAM by 2027, reinforcing convergence with EU pricing.

- China operates the world’s second-largest carbon market through its National ETS, currently covering more than 2,000 power sector entities representing roughly 4.5 billion tonnes of CO₂ emissions. The system is expanding to include steel, cement, and aluminium, integrating carbon pricing across key industrial sectors. Although prices remain relatively modest (around CNY 60–80 per tonne, or USD 8–11), the scale and rapid institutional development make China a central pillar of the global carbon-pricing landscape.

- Australia relaunched its Safeguard Mechanism - DCCEEW, setting declining emissions baselines for major facilities and allowing compliance through ACCUs, revitalising a once-nascent market.

- Although ACCU prices have remained relatively flat in recent years, rising compliance activity is expected to drive stronger demand for carbon permits. According to Commonwealth Bank research, modelling by the Australian Treasury likely overestimates the adoption of low-carbon technologies (CBA, 2025,). As a result, carbon credits are expected to play an important role in offsetting excess emissions from safeguard facilities aiming to achieve the annual emissions intensity reduction target of 4.9% through to 2030.

- Core Markets projects that demand for ACCUs will reach its peak in 2034, with prices expected to rise steadily each year until then (Core Markets, 2025). By that stage, the stronger price signal is anticipated to shift incentives toward physical decarbonisation rather than reliance on offsets.

Together, these regimes form a connected price corridor that increasingly defines global competitiveness. For investors, carbon cost is no longer a regional anomaly; it has become a pervasive cross-asset risk factor embedded in valuations and trade.

Figure: A world map highlighting ETS coverage (~28 % of global GHG), with callouts for EU, UK, and Australia.

Source: https://www.worldbank.org/en/publication/state-and-trends-of-carbon-pricing

Graph: Carbon pricing schemes

Source: World Bank, Clean Energy Regulator

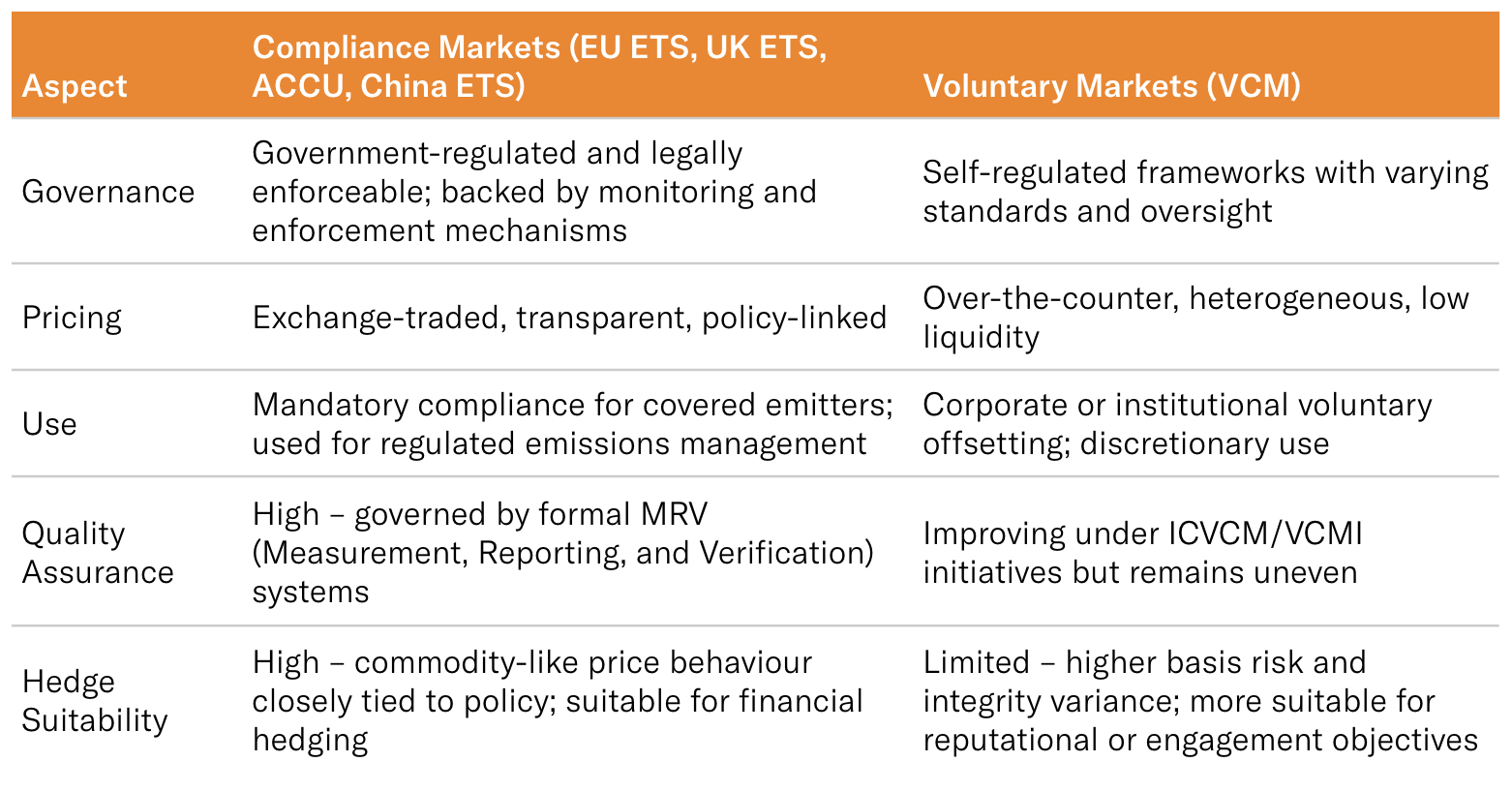

2.2 Market structure and maturity

2.2.1 Market structure and maturity

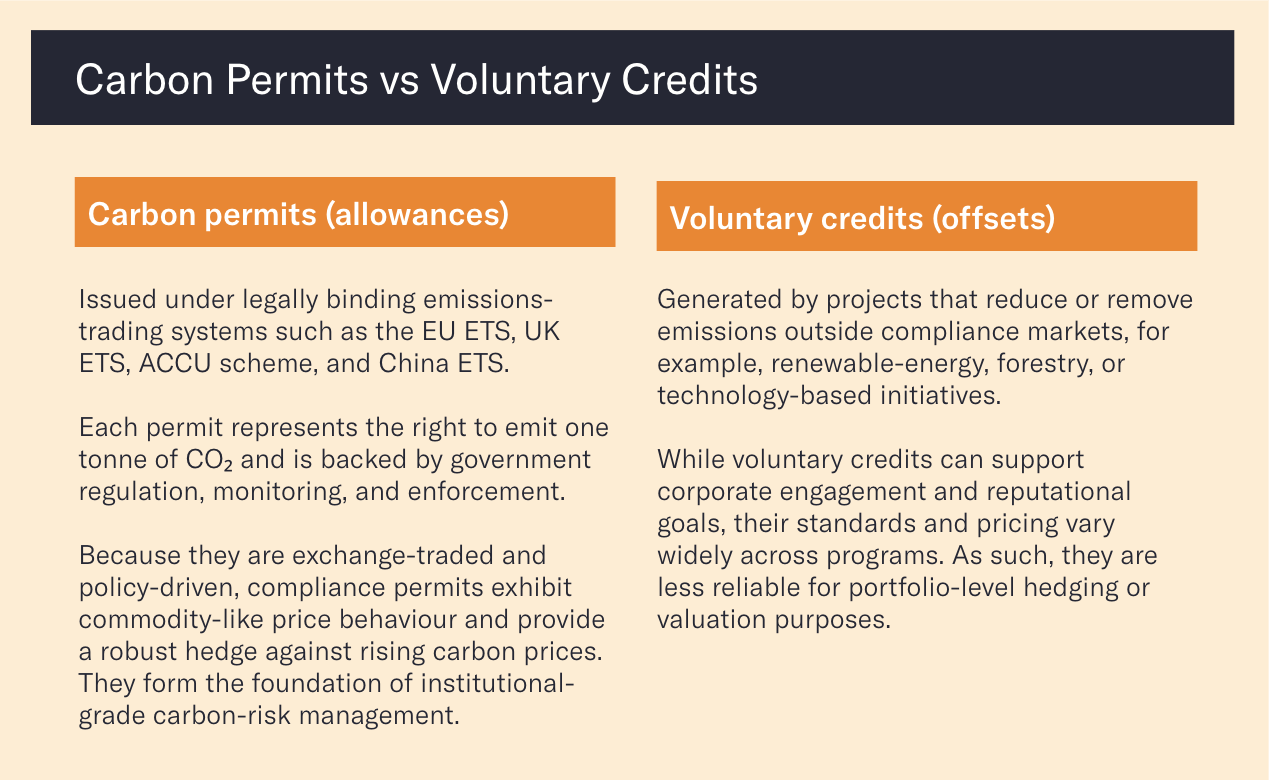

Compliance markets differ markedly from voluntary systems. They are legally binding, exchange-traded, and backed by government monitoring and enforcement, which gives them the liquidity, transparency, and price integrity necessary for institutional use.

Voluntary markets, by contrast, remain fragmented, though governance and quality standards are improving under the Integrity Council for the Voluntary Carbon Market (ICVCM) and the Voluntary Carbon Markets Integrity Initiative (VCMI).

Within compliance systems, correlations between instruments are strengthening as policies align, a key enabler for cross-market hedging strategies. For example, historical correlations between European Union Allowances (EUA) and United Kingdom Allowances (UKA) exceed 0.8, providing meaningful hedge effectiveness across European exposures.

Compliance permits

Compliance permits function as regulated financial instruments suited to managing transition risk.

Voluntary credits

Voluntary credits, while valuable for demonstrating climate ambition, are best viewed as complementary tools rather than core hedging assets.

2.2.1 Voluntary vs Compliance Markets

2.3 Why carbon pricing matters for investors

Rising carbon prices translate into real, quantifiable financial risk. They influence:

- Operating margins of emissions-intensive sectors;

- Asset valuations through discounted-cash-flow adjustments;

- Cost-of-capital differentials as financiers re-price risk; and

- Equity and bond performance as market expectations shift.

Emmi’s analytics link these price pathways directly to portfolio exposure, enabling investors to estimate how a €50 increase in carbon price could translate to a specific reduction in portfolio value, and how strategic credit holdings can offset part of that erosion.

3.0 The Case for Hedging Transition Risk with Carbon Credits

Institutional investors now increasingly recognise that transition risk is not a distant externality; it is a pricing variable being embedded in capital markets. Carbon-intensive assets face valuation pressure as global policy converges around decarbonisation targets. Yet divestment alone cannot entirely eliminate exposure. The challenge is to manage these risks dynamically, in the same way investors manage currency or interest-rate risk.

Carbon credits, when treated as a regulated commodity rather than a philanthropic offset, offer a financial instrument to hedge exposure to rising carbon prices. They can help neutralise part of the loss that a carbon-intensive portfolio would experience as the cost of carbon increases.

However, this only works when the hedge is built on a clear analytical foundation, understanding how much carbon exposure exists in the portfolio, how sensitive it is to price changes, and which credits most closely track those prices.

3.1 Quantifying exposure: From emissions to financial risk

The first step is quantification.

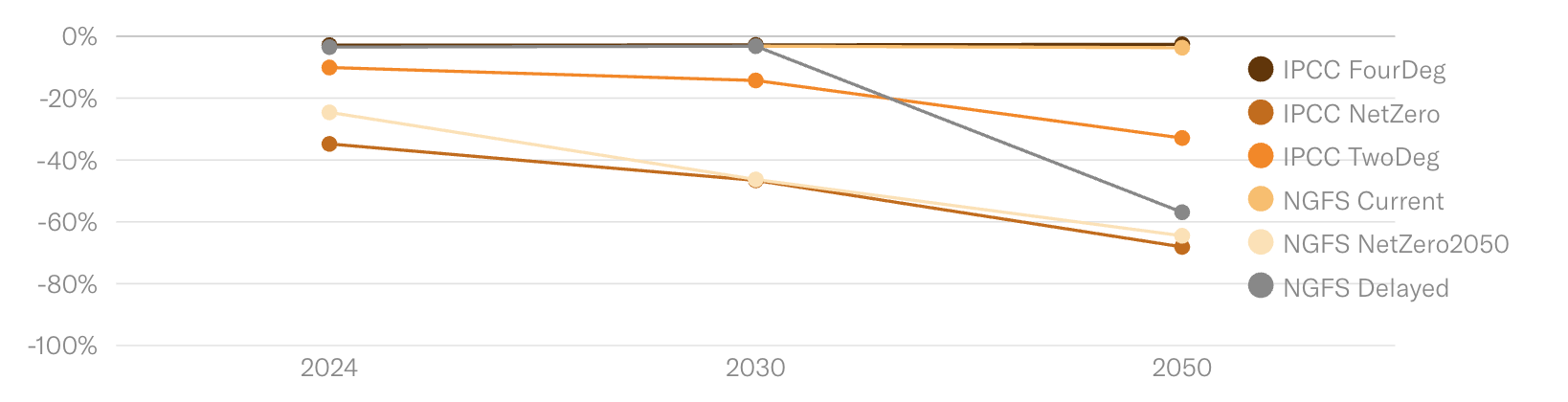

Carbon Diagnostic’s analytics convert a portfolio’s underlying emissions exposure into a financial metric known as Potential Carbon Liability (PCL), the estimated value erosion a portfolio would experience under a given climate scenario and its associated carbon-price pathway. This bridges the language of sustainability and finance, allowing portfolio managers to treat carbon as a measurable risk factor.

PCL is scenario-based, flexible, and compatible with standard return models. It can be calculated across asset classes and geographies, enabling comparison between all assets, and credit portfolios.

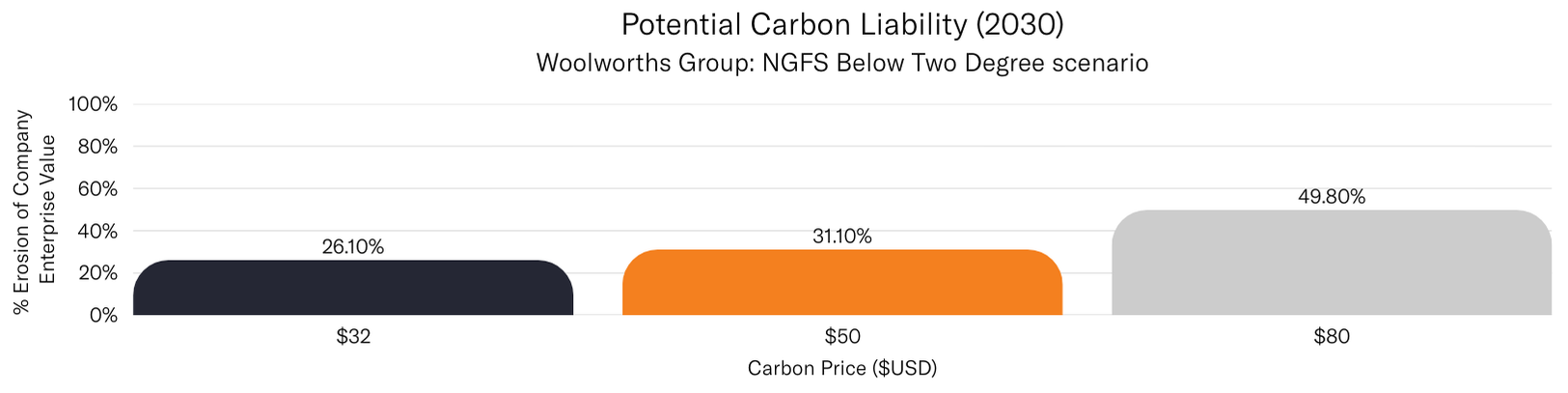

Graph: PCL across climate scenarios (FTSE100)

Once quantified, the question becomes: how can that liability be managed?

3.2 Two functional uses of carbon credits

Emmi’s research distinguishes between two distinct applications of carbon credits in portfolios:

Financial-hedging use:

Holding credits as tradeable assets provides a position that rises in value as carbon prices increase, directly offsetting potential valuation losses in carbon-exposed holdings.

Temperature-alignment use:

Retiring carbon credits (offsets) to offset financed emissions improves reported temperature alignment, signalling progress toward net-zero objectives.

Temperature alignment vs value hedging

Temperature alignment focuses on reported climate metrics; value hedging focuses on protecting portfolio returns. Both are valid, but serve different purposes.

3.3 Basis risk and market selection

As with any hedge, basis risk, the mismatch between the hedge instrument and the underlying exposure, is critical.

Voluntary-market credits can diverge in price and integrity; compliance-market instruments, such as EUAs, UKAs, CAs, and ACCUs, more closely track the policy-driven carbon price embedded in corporate valuations.

In practice, aligning compliance credit exposure with the jurisdictions of portfolio holdings reduces basis risk and ensures that carbon-price signals correspond to the relevant policy environments.

3.4 Integration into portfolio construction

Once exposure is quantified and hedge instruments selected, the implementation mirrors any other risk-management process:

- Determine Hedge Ratio

Number of tonnes (permits or allowances) required to offset portfolio carbon exposure under a chosen scenario. - Select Market Instruments

E.g., EUAs, UKAs, ACCUs, or blended baskets. - Monitor and Rebalance

Adjust positions as portfolio composition or carbon prices evolve. - Integrate Reporting

Link hedging activity to climate disclosures (TCFD, ISSB, SFDR) without conflating financial and emissions claims.

Treating carbon credits as a recognised asset class within portfolio-risk systems enhances transparency and supports investment-committee governance.

4.0 How a Carbon-Credit Hedge Works in Practice

Emmi has worked with institutional clients to demonstrate two complementary approaches to hedging portfolio transition risk using carbon credits.

The objective in each case is the same: to quantify potential value erosion under rising carbon-price trajectories and design a hedge that mitigates exposure while maintaining investment discipline.

Step 1: Baseline transition-risk analysis

Carbon Diagnostics establishes the baseline: financed emissions, temperature alignment, and the portfolio’s carbon-budget overspend under a defined scenario.

This analysis translates directly into Potential Carbon Liability (PCL), the percentage of portfolio value at risk if policy tightening drives carbon prices along that path.

This baseline provides the quantitative foundation for constructing either a financial hedging position or a temperature alignment strategy.

Step 2: Modelled carbon-price pathways

Using Carbon Diagnostics data and regional carbon-pricing forecasts, investors can model the impacts on portfolio valuation under a range of policy and technology scenarios through 2030 and 2050.

This identifies both the scale of potential downside risk and the sensitivity of portfolio value to changes in carbon-price trajectories.

Step 3: Applying the carbon-permit (allowance) hedge

Carbon-credit hedging can be implemented through two distinct but complementary pathways:

Held-for-sale hedge – Financial exposure management

Credits or allowances are held as tradable assets whose value rises with carbon prices.

When treated as available-for-sale instruments, these positions function much like commodity exposures, directly offsetting the potential loss that a carbon-intensive portfolio may experience as compliance costs increase.

Because compliance-market instruments (such as EUAs, UKAs, ACCUs and NZUs) are exchange-traded and policy-linked, they closely track the regulatory price signal that drives transition risk, making them suitable for portfolio-level hedging.

Typical sensitivity tests show that an appropriately sized held-for-sale position can materially reduce Potential Carbon Liability without compromising portfolio returns.

Retired-credit hedge – Temperature alignment and permanent abatement

An alternative pathway is to retire credits once purchased, permanently removing them from circulation. Retirement ensures that the emissions reduction or removal associated with each credit is claimed only once, strengthening the connection between capital allocation and real-world decarbonisation.

For investors, retiring credits rather than trading them reduces available supply, supports portfolio temperature alignment, and provides a clear demonstration of progress toward net-zero goals. Many institutions formalise this approach through an annual retirement budget calibrated to financed-emissions targets.

Using compliance-grade or high-integrity removal credits for retirement offers a measurable and verifiable method to reduce financed emissions while maintaining transparent governance and reporting.

These two applications serve different purposes: the held-for-sale hedge manages value exposure to policy-driven price risk. In contrast, the retirement hedge strengthens climate-alignment metrics and long-term transition credibility.

Step 4: Ongoing monitoring

Transition risk evolves as regulation, market prices, and portfolio composition change.

Emmi’s analytics enable investors to regularly recalculate portfolio alignment and PCL, ensuring that both financial and retirement hedges remain appropriately calibrated.

Firms can integrate these updates into governance cycles, investment-committee materials, and stakeholder reporting, maintaining transparency on the dual dimensions of financial and climate performance.

Regular recalibration using current data helps investors maintain proportionate, credible, and aligned hedging strategies as transition dynamics shift.

Illustrative outcomes

Institutional portfolios that incorporate carbon-hedging typically achieve three core outcomes:

Reduced value erosion, achieved through holding compliance-market permits as tradable financial hedges against rising policy-driven carbon prices.

Improved temperature alignment, delivered when high-integrity credits are retired annually to match financed-emissions targets.

Enhanced transparency and governance, supported by scenario-based reporting that links hedging activity to fiduciary objectives.

Key success factors for institutional carbon-hedging

Quality of instruments

Preference for compliance permits or high-integrity removal credits.

Quantitative foundation

Use of PCL and temperature-alignment analytics to size exposures accurately.

Governance clarity

Document intent, held for sale vs retired, to avoid double-counting.

Monitoring

Integrate both hedges into ongoing performance and climate-risk reporting.

Working Example

Apostle white paper - Building a climate-resilient portfolio without compromising returns

5.0 Integrating Carbon Credits into Portfolio Strategy

Carbon instruments, including permits and credits, are often viewed as the final step in a sustainability strategy. In practice, they should be considered an integral part of portfolio construction and risk management. When treated as a legitimate financial asset, credits can enhance diversification, improve downside protection against transition shocks, and signal a disciplined approach to climate governance.

Beyond this, as the integrity of global carbon markets strengthens and baselines tighten, the potential for capital appreciation in carbon credits merits inclusion within a diversified portfolio.

5.1 Strategic portfolio applications

Carbon credits can support three complementary strategic goals:

- Risk mitigation

Hedging expected carbon-price increases reduces potential value erosion, particularly for portfolios with heavy industrial, materials, or energy exposure.

- Transition positioning

Allocating to carbon-credit funds or indexes gives exposure to an emerging asset class likely to appreciate as global policy tightens.

- Stakeholder alignment

Using credits to improve temperature alignment or demonstrate measurable progress toward net-zero targets reinforces fiduciary credibility and regulatory compliance.

Investors who model both the 'temperature-alignment' and ‘financial-hedging’ cases can transparently show boards and regulators how each use supports distinct objectives.

5.2 Governance and disclosure alignment

Regulatory frameworks such as TCFD, ISSB S2, ESRS E2 and SFDR now require investors to disclose transition-risk management. Demonstrating a quantitative methodology for assessing and mitigating carbon exposure positions investors ahead of compliance requirements.

Integrating carbon-price sensitivity and hedging analytics into strategic-asset-allocation reviews reframes climate action from an ESG gesture into a fiduciary necessity.

6.0 Market Outlook and Investor Implications

The next five years will define the shape and scale of global carbon markets. With carbon-pricing instruments now covering roughly 28 % of global emissions, generating over USD 100 billion in annual revenue and set to expand. Policies are converging, new sectors are entering compliance systems, and voluntary markets are undergoing an integrity reset. For institutional investors, this evolution presents both transition risk and alpha opportunity.

6.1 Emerging market and technology trends

Removals premium

High-integrity removal credits (biochar, direct air capture, mineralisation) already trade at multiples of avoidance projects, reflecting demand for permanence.

Digital measurement and verification

Satellite data, IoT, and blockchain registries are increasing transparency and liquidity.

Financial product innovation

New indices, futures, and tokenised credits are turning carbon into a standardised investment exposure.

Corporate demand

Mandatory transition-plans legislation (EU CSRD, UK Transition Plan Taskforce) will drive sustained credit demand from heavy industry and finance.

6.2 Investor implications

- Transition risk is now quantifiable

Metrics such as PCL enable measurement and comparison of carbon exposure in the same language as credit or duration risk.

- Hedging is cost-effective insurance

Allocating a small share of portfolio value to compliance-market carbon credits can meaningfully reduce downside exposure under tightening policy scenarios.

- Carbon markets offer diversification and return potential

The secular trend toward higher carbon prices creates long-term appreciation prospects in regulated credit instruments and funds.

- Data and integrity will differentiate managers

Investors equipped with transparent, scenario-based analytics, such as Carbon Diagnostics, will be able to demonstrate alignment and defend strategy decisions to boards and regulators.

6.3 Long-term outlook

The next phase of carbon markets will see integration across systems, expansion into new sectors, and convergence of compliance and voluntary standards. As this occurs, carbon will solidify as a core macro-risk factor influencing asset allocation alongside inflation, interest rates, and currency.

Early adoption of quantitative carbon-risk tools allows investors to manage exposure proactively rather than reactively, turning compliance cost into competitive advantage.

7.0 The Fiduciary Imperative for Transition-Ready Portfolios

Institutional investors are facing a structural redefinition of fiduciary duty.

What was once interpreted narrowly as maximising financial returns now necessarily includes managing exposure to systemic climate risk.

As carbon pricing, disclosure standards, and policy frameworks accelerate, climate transition risk is no longer a peripheral ESG issue, it is a core financial consideration.

7.1 Transition readiness as financial prudence

Transition risk is now directly visible in earnings, credit spreads, and asset valuations. For institutional investors, managing this exposure is not a matter of sustainability preference, but a fiduciary obligation.

Portfolios equipped with quantified carbon-risk metrics and credible hedging strategies, such as those demonstrated in the Apostle case, are better positioned to protect value as policy frameworks tighten and carbon costs rise.

Integrating carbon analytics into investment governance ensures that transition management is treated with the same rigour as credit, duration, or currency risk.

7.2 Transition risk as a recognised financial factor

Carbon exposure has become a measurable component of financial performance and asset allocation. As carbon pricing expands across jurisdictions, policy-driven price trajectories are influencing earnings, capital flows, and valuations much like other macro-risk variables such as interest rates or inflation. Integrating carbon-risk metrics, including Potential Carbon Liability (PCL) and temperature-alignment measures, enables investors to assess and manage this exposure consistently across portfolios, positioning transition readiness as a standard element of financial risk management.

7.3 The role of carbon credits in the toolkit

Carbon instruments (permits and credits) are not substitutes for decarbonisation; they are instruments that help investors manage the pace and impact of the transition. When applied systematically, compliance-market credits can serve dual purposes:

Financial hedging: Offsetting value erosion from rising policy-driven carbon prices.

Temperature alignment: Supporting verifiable progress toward net-zero commitments through the retirement of high-integrity credits.

Used together within a transparent, data-driven framework, these instruments provide flexibility for portfolios that cannot immediately divest, enabling investors to manage transition exposure while maintaining fiduciary discipline.

Conclusion: From Awareness to Action

The decarbonisation of the global economy is not a matter of ideology; it is a financial inevitability.

For investors, the question is not whether transition risk exists, but how effectively it is measured, managed, and mitigated.

Carbon credits, particularly those from compliance markets, have evolved into credible financial instruments that can play a meaningful role in that process.

When integrated through robust analytics such as Carbon Diagnostics, credits can help institutional investors:

- Quantify their exposure to carbon-price risk,

- Hedge potential value erosion,

- Improve portfolio alignment with global temperature goals, and

- Demonstrate proactive fiduciary governance.

There is no single path to net zero. But there is a clear path to resilience: measure, model, and manage carbon risk as a core portfolio factor.

Investors who adopt that discipline today will be better prepared for the economic realities of tomorrow’s carbon-constrained world.

Authors

Skye Frugte

GCertBus | MFin (Sustainable Transitions Track)

Callum Thompson

B AdvFinEcon(Hons)

Download the full document

Stay in the know. Subscribe to updates

Find out about our latest developments, and get our research reports first.