Sector Analysis

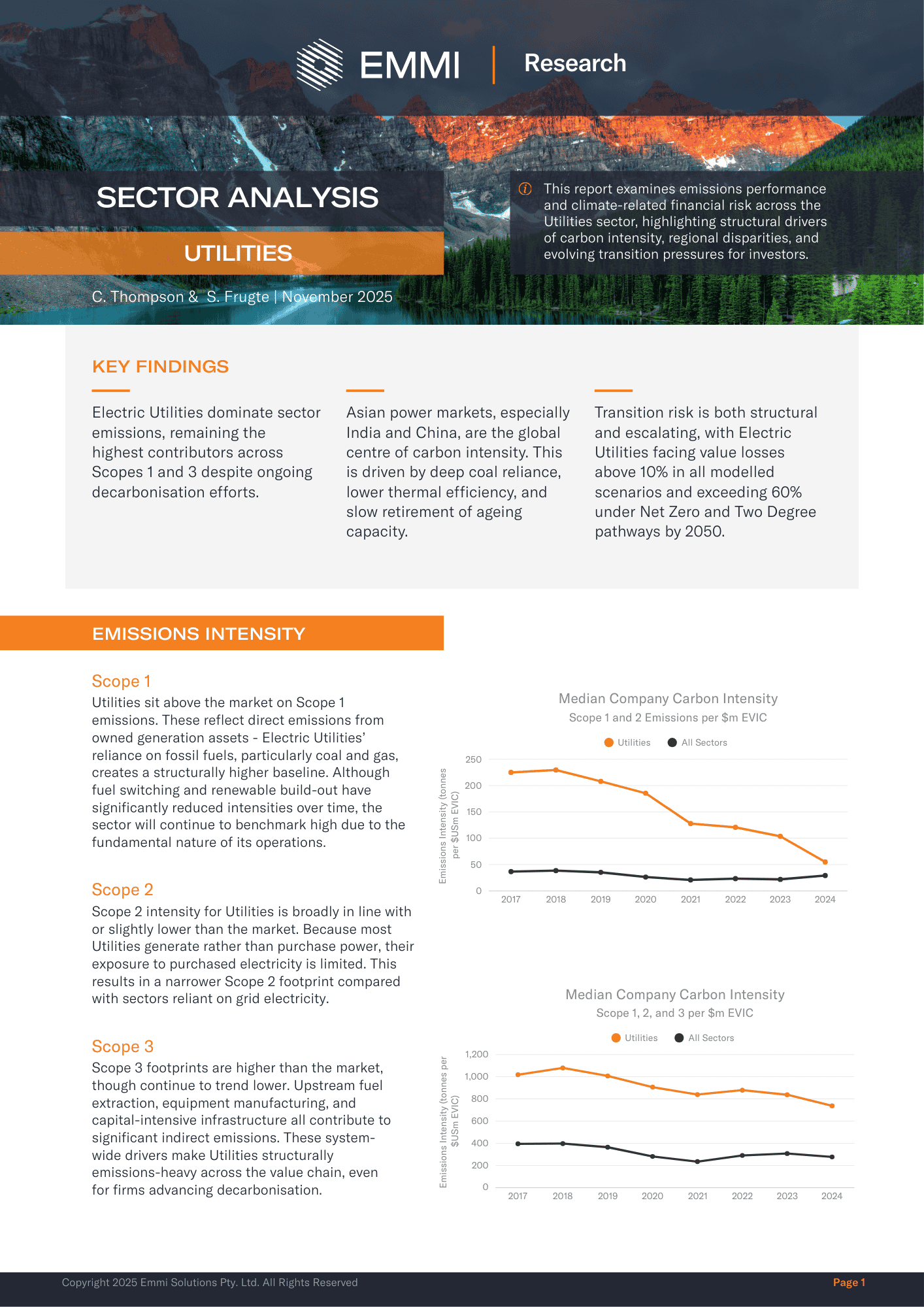

The Utilities sector remains structurally emissions-intensive relative to the broader market, particularly within Electric Utilities. While renewable deployment has reduced carbon intensity over time, fossil-based generation assets continue to anchor operational and value-chain exposure.

Regional dispersion is pronounced. India exhibits the highest average carbon intensity across major markets, with coal accounting for around 60% of generation and demand projected to more than double over the next decade. Coal-fired generation in India is now expected to peak in the early 2040s, despite a net-zero target of 2070.

Transition risk is material across all scenarios. Electric Utilities face average Value at Risk above 10%, rising beyond 60% under Net Zero and Two Degree pathways by 2050. For investors, the sector’s carbon profile is not simply an environmental metric; it is also a question of capital allocation and long-duration asset risk.

Download the full document

Stay in the know. Subscribe to updates

Find out about our latest developments, and get our research reports first.