Disclosure Is Not Delivery: Testing Australia's Largest Resource Companies Against Their Own 2030 Targets

When you apply Emmi's Targets and Forecasts data to your holdings, the results may not be what you expect. The gap between a company's published 2030 commitment and its actual emissions trajectory is not always what investors assume. For many investors, that gap has prompted a closer look at specific holdings, particularly in markets where regulatory expectations around target-setting are tightest, including the EU.

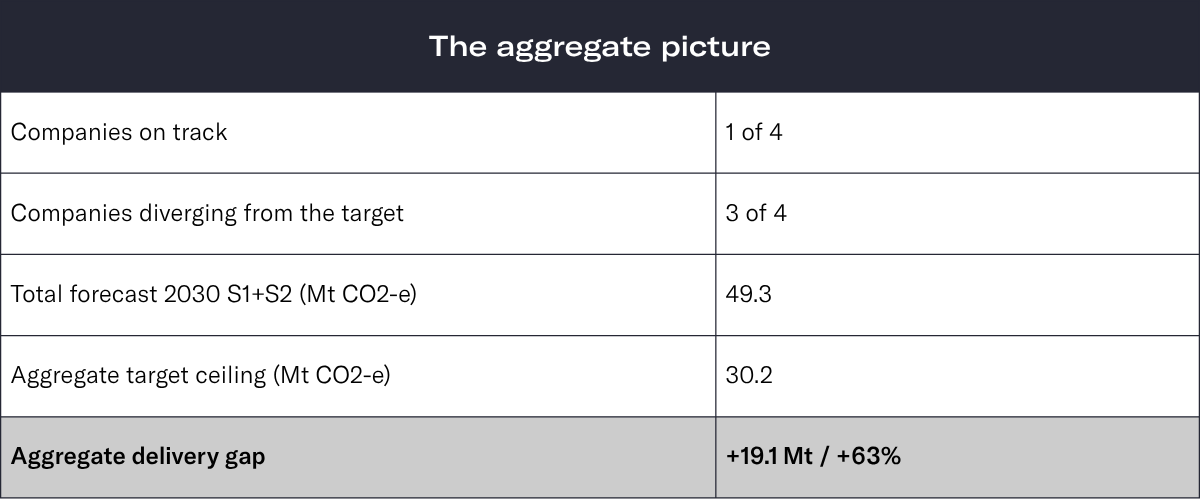

Emmi applied the same framework to four of Australia's largest listed resource companies and found the same pattern.

Most transition risk frameworks score companies on what they disclose. Target year, percentage reduction, baseline year, scope coverage. The presence of a 2030 commitment is treated as evidence that the company is on the path.

The frame is incomplete.

The right question is not whether a target exists, but whether the realised emissions trajectory is consistent with the commitment. Across BHP, Rio Tinto, Fortescue, and Woodside, the aggregate forecast 2030 Scope 1 and 2 emissions sit 63% above the implied target ceiling. Only one of the four shows a trajectory consistent with its stated commitment.

Disclosure is not delivery. Three of the four major Australian resource companies have a 2030 commitment that the current emissions trajectory does not support.

Why these four companies matter to your portfolio

BHP, Rio Tinto, Fortescue, and Woodside are not edge cases. They are four of the largest companies on the ASX by market capitalisation and among the heaviest emitters in the Australian listed equity universe. For any institutional investor with Australian equity exposure, superannuation funds, sovereign wealth funds, or diversified mandates, these names are almost certainly present in the portfolio. Collectively, they account for a significant share of the financed emissions in the Australian large-cap resource book. What happens to their transition risk exposure is not a niche question. It is a portfolio question.

How Targets and Forecasts works

Emmi's Targets and Forecasts data produces a bottom-up, gross projection of Scope 1, 2, and 3 emissions and maps those projections against each company's stated SBTi-aligned commitments. The framework combines four inputs:

- Reported historical emissions at facility, asset, and entity level (vintage FY2015 through FY2025)

- Production and revenue drivers at the sector and sub-sector level

- Sanctioned capex and project-pipeline signals were disclosed

- A stochastic projection returning a forecast mean and standard deviation to 2030

The model does not assume offsets, retired carbon credits, or unannounced abatement. It captures sanctioned production growth as reported by the companies. Where a company has executed disclosed abatement and the effect has shown up in realised emissions, the forecast reflects it. Where a company has announced a project but realised emissions have not moved, the model does not bake in future delivery.

This is what makes Targets and Forecasts useful as a delivery test. The target is the destination. The forecast is the trajectory implied by the current data.

This analysis covers Scope 1 and 2 emissions, reflecting the data available for these companies at the time of publication.

Company-by-company: where the trajectories land

BHP. On track.

BHP's 2030 target is a 30% reduction in Scope 1 and 2 emissions from an FY2020 baseline of 13.6 Mt, giving a target ceiling of 9.5 Mt. The forecast for 2030 is 5.4 Mt: 43% inside the ceiling.

BHP had reported a 32% reduction by FY2024, and the forecast model extrapolates that run-rate forward. Renewable PPAs across Pilbara operations, Escondida desalinated power, and fleet electrification have shown up in realised data.

The engagement implication: the disclosure-delivery gap on operational emissions is small. Stewardship focus should shift to Scope 3, where BHP's value chain emissions of 378 Mt in FY2025 dwarf the operational figure and the target framing is materially weaker.

Rio Tinto. 67% above target.

Rio Tinto's 2030 target is a 50% reduction from a 2018 baseline of 32.6 Mt, giving a target ceiling of 16.3 Mt. The forecast is 27.3 Mt: 67% above that ceiling.

The company has committed approximately US$7.5 billion of decarbonisation capex through 2030, covering the ELYSIS inert anode programme, smelter electrification, and renewable PPAs in Queensland and Western Australia. By the end of 2023, reported emissions had fallen only 6% from the 2018 baseline. The forecast captures that realised trajectory, not the projected delivery of uncommenced projects.

The forensic engagement question: which capex commitments are FID-confirmed and on schedule, and which remain conditional on technology not yet demonstrated at production scale?

Fortescue. Largest ambition, largest gap.

Fortescue's target is absolute zero Scope 1 and 2 emissions from its Australian iron ore operations by 2030: the Real Zero target. The forecast is 4.9 Mt. The target is zero. The full forecast figure is the gap.

The forecast model projects Scope 1 emissions rising by 44% from FY2025 to FY2030, driven by production growth and the absence of abatement implemented in realised emissions. Fortescue committed US$6.2 billion to electrification and green hydrogen capex in September 2022. As of FY2025, that capex has not translated into reported reductions at scale.

The engagement case: can a complete decarbonisation trajectory be compressed into the back half of this decade? The battery-electric locomotive commissioning milestones in 2025 are the nearest testable interim signals.

Woodside. 164% above target.

Woodside's 2030 target is a 30% net reduction in equity Scope 1 and 2 emissions from a 2016-2020 average of 6.27 Mt, giving a net target ceiling of 4.39 Mt. The forecast is 11.6 Mt gross: 164% above the net ceiling.

Sangomar (Senegal), Scarborough (Western Australia), and Trion (Mexico) all ramp through the forecast horizon. Woodside's 2025 disclosure claims a 15% net reduction, achieved with material offset volumes. The forecast model is gross and does not net offsets, so the directional gap reflects both perimeter differences and underlying production growth.

The engagement implication: investors need to determine whether net targets backed by offsets are equivalent to gross reductions. If they are not, the disclosure-delivery gap on Woodside is the largest in this set on a like-for-like basis.

The aggregate picture

What this means for Transition Value at Risk

Transition Value at Risk under a 2°C-aligned scenario is a function of residual emissions a company carries through the transition. Two companies with the same starting point and the same stated target produce very different TVaR profiles depending on whether the realised path tracks the target or diverges from it.

The structural intuition comes from the Maersk SBTi case: when the realised trajectory matches the validated target, Transition Value at Risk collapses toward zero. When it diverges, it approximates the business-as-usual case minus avoided costs of unbuilt abatement.

Applied to this set, BHP's BAU and target-aligned Transition Value at Risk converge. For Rio Tinto, Fortescue, and Woodside, BAU Transition Value at Risk materially exceeds target-aligned Transition Value at Risk. The delta is the financial value of unexecuted abatement: the unpriced cost sitting in the Australian large-cap resource book.

The operational shift for stewardship teams

The data changes what stewardship engagement looks like in practice. The question moves from 'does the company have a target?' to three more specific questions:

- What is the implied target trajectory? Convert the percentage target into an absolute tonnage path with annual milestones. Most disclosures provide the endpoint, not the path.

- Where does the forecast diverge from the implied path, and by how much? The gap quantifies the engagement priority.

- What are the testable interim signals? Capex execution dates, project commissioning milestones, and reported emissions vintages are the checkpoints between now and 2030.

When these three are answered, escalation becomes data-driven. The question shifts from whether a company has committed to whether it is delivering. That is the only question that matters before 2030. Emmi's Targets and Forecasts data was built to answer it.